By Ediri Asher Unoroh

The phrase smart contracts might be a tad complicated if you are new to the world of blockchain and crypto asset management. But if’ smart contracts’ are the cornerstone on which Defi will work or invariably works, then it only makes sense for everyone to know what they are exactly.

One of the best ways to know what smart contracts are is to understand their origin. Unknown to a lot of folks, the term ‘smart contracts’ has been around long before the advent of the first cryptocurrency in the world – Bitcoin.

The origin of smart contracts

Sometime around the early 1990s, long before the major adopters of this technology, the Gen Z’s started making it into the world, a lawyer who doubled as a computer scientist and cryptographer, Nick Szabo started talking about smart contracts.

You can expect that these talks didn’t resonate with the broader community at that time as it does now with the immense popularity that blockchain and the technologies anchored on it such as DeFi currently enjoy.

A lawyer, Nick Szabo was particularly wary of the fact that contracts could only be enforced by the traditional governments thereby making them expensive and unreliable. As such, he developed smart contracts with the goal of bringing “highly evolved practices of contract law and practice to the design of electronic commerce protocols between strangers on the Internet.”

So what exactly are smart contracts?

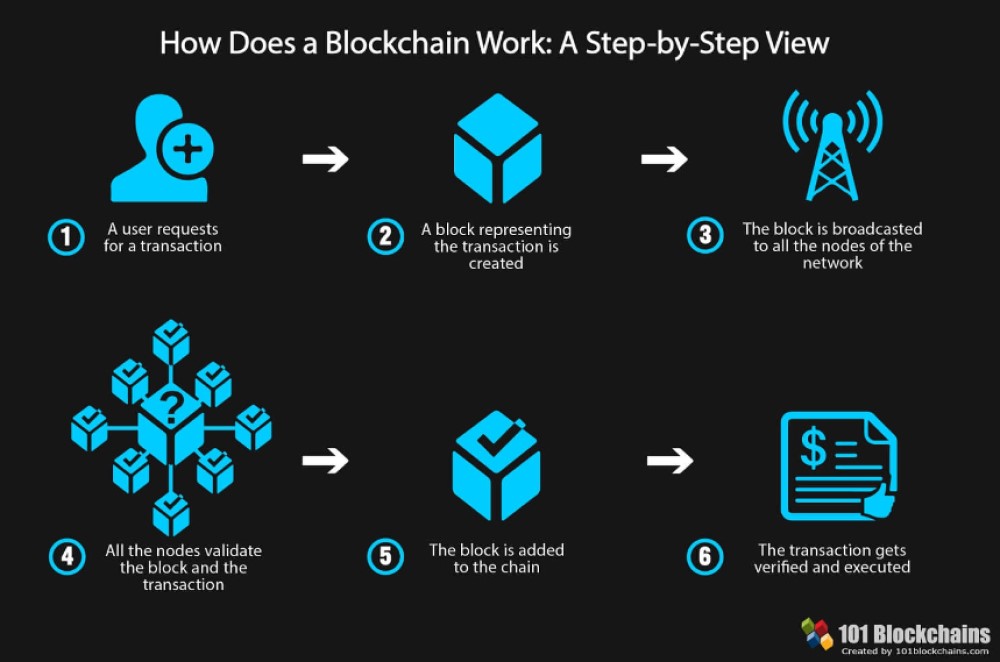

Smart contracts are pieces of code that exist on the blockchain. Remember the blockchain? Blockchain is simply that system of documenting information in a way that makes it impossible to change or even cheat the system.

The first thing you must know about ‘smart contracts’ is that they are characterized by three things. The first is that everyone can see them. Secondly, they can’t be changed or tampered with. Lastly and most importantly, they are able to execute themselves without third party intervention, rogue or otherwise.

So if I agree to send 1,000 satoshis to Mr Pinky Brain’s wallet every day for 10 days, the job of the codes – or smart contracts- will be to ensure that the agreement to send that coin is executed without fail.

The smart contract also ensures that Mr Pinky keeps to his end of the agreement. Let’s say in this case he is to help me build a digital robot army that is programmed to help me achieve world domination.

With ‘smart contract’, Mr Pinky Brain will not need to get the courts involved to make sure I keep to my end of the bargain.

The job of the smart contract is to be the undying incorruptible judge and the enforcing authority.

‘Smart contracts’ have never been made this simple, yeah? I know!

So you see, the purpose behind the idea of ‘smart contract’ is so that we can embed specific contractual provisions or clauses in the hard and software we deal with now and in the not so distant future.

The end result here is that we make the breach of contracts outrightly impossible or ridiculously expensive.

Preventing fraud and disrupting business

In summary, what smart contracts do is guide the execution of transactions without any third-party input. The processes are automated; the transactions tractable and can easily act as proxy for legal contracts.

Smart contracts are the future of contracts. And the use cases – real-life application – will change the way we do everything in the very inefficient servicing culture we have in Africa.

I have been in finance for the last 6 years of my life and I can tell you for free how unreliable contractile agreements are in Africa; from debt access, debt servicing, repayment, insurance provisions and investment returns.

The financial services industry stands to be one of the biggest benefactors in the mass adoption of smart contracts on the blockchain, from insurance companies to banks and fintechs.

Even non stem companies like organisations in the legal and asset management sectors will be totally disrupted by its adoption and application.

A prime example of this is the management of wills after a person is deceased. In Africa this is often a very contentious affair that sometimes leads to needless fatalities and time consuming court appearances by concerned parties over the estate of the deceased.

We’ve seen families contest wills with legal proceedings lingering on for years with all parties of interest expending vast resources for the cases.

However, all these can be avoided if the deceased has a smart contract issued beforehand. With a smart contract, the deceased can automate the process and complete execution even without the input of lawyers and notaries.

For example, he or she can prepare a smart contract that distributes his or her assets once he or she passes.

How smart contracts work

The deceased can set it up in such a way that every 30 or 60 days, he or she inputs a digital key on the blockchain to prove that they are still alive and of sound mind.

If they fail to input the keys as written on the smart contract, the assets in the estate are automatically dispensed to the dependents or beneficiaries as signified in the smart contract.

The smart contract simply executes what was allocated by the owner of the estate. That way we avoid a Nollywood story.

Simple as ABCD.

Financial services can also build their products on the blockchain with smart contracts as back bone and executors. Users can borrow fiat or even crypto using their coins as security for the loans. This will immediately lower default transactions in their books.

Many financial services companies have gone bankrupt and out of business as a result of nonperforming loans. Smart contracts can help with this.

With ‘smart contract’ these loans are monitored and penalties affected if there is a default on the part of the user.S o users forfeit their cryptocurrency or NFT ownership in the event that the facility is no longer performing.

Governments in Africa need disruption in their operations. In the near future, I see the government using smart contracts to help automate operations thus becoming more efficient, reliable and transparent. This is because with smart contracts you get to see all the details on the decentralized blockchain.

Smart contracts can also be used by the government for their census exercises, regional data collection and the almighty elections that are regularly plagued with everything the blockchain stands against; from transparency to agency efficiency to speed and cost reduction.

With smart contracts we can say bye to multiple duplicities at the polling stations, underage voting and the wanton violence that fraught the electoral process here in Africa.

The possibilities are endless and the advantages for us here in Africa are mindblowing because of blockchain and the smart contract.

Ediri Asher Unoroh is a Bitcoiner from Africa building technology for Defi and Web3. He handles Product Development at Safi, a crypto service and DCA platform.

Twitter : @Asheroflagos