The battle to get middle-aged and older Nigerians to write wills or communicate their investments to their next of kin has not been won. With the rise of fintech, another battle is being waged.

As fintech offers investment opportunities for young Nigerians, a recent poll by Technext shows that they too, like their parents, don’t have wills and haven’t told their next of kin of all their investments.

For many people having a will is a good idea. Making a will helps your heirs, or next of kin, avoid unnecessary hassles.

Though no single document will likely resolve every issue that arises after your death, a will—officially known as a last will and testament – can come pretty close.

Many young Nigerians don’t have wills

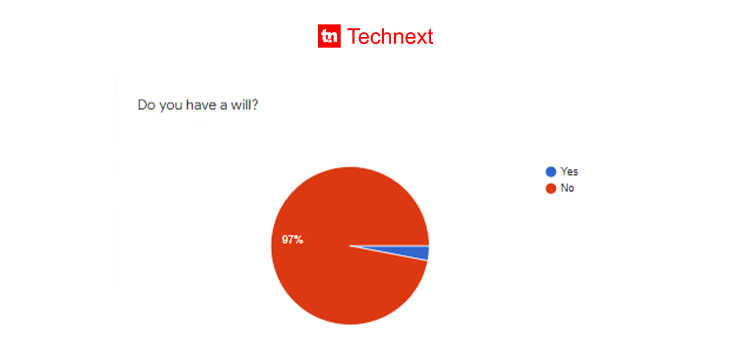

The result from a recent poll on young Nigerians between 23 to 35, who have all completed their national youth service, shows that 97 per cent of young Nigerians don’t have a will. While only three per cent have wills.

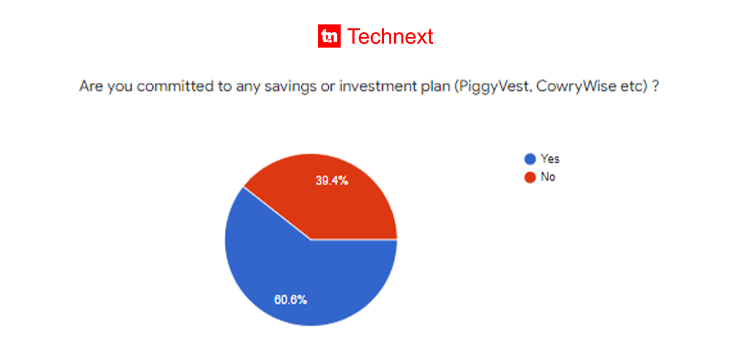

60.6 per cent of them say they are committed to a savings plan or investment with a fintech. And, without the existence of a will that explicitly states who should inherit a person’s property, they (the property) ideally transfer to the next of kin.

But as young Nigerians begin this early-stage investment, many, like their parents, are without wills and have failed to bring their next of kin up to speed with all their investment and savings plans.

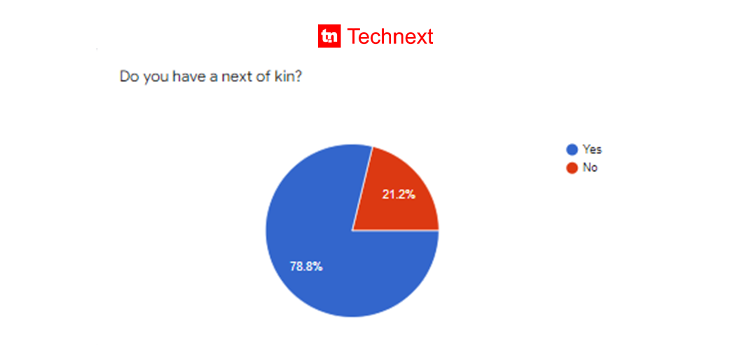

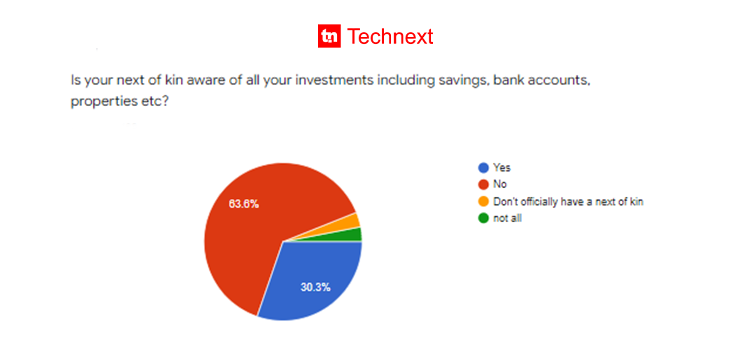

78.8 per cent of the poll participants say they do have a next of kin. But, 63.6% say their next of kin is not aware of all their savings and investment plans.

NCC projects that the value of the Nigerian fintech industry will rise to $543.3 million this year, an indication of rapid growth in the sector.

With this boom, young Nigerians are buying into investment and savings plans, including cryptocurrency and NFTs. While this is an obvious sign of progress, the above Technext poll shows that the stage is gradually being set for a repetition of the sins of the fathers.

The CBN’s word on dormant accounts

In Nigeria, the Central Bank’s provision on dormant accounts and for the next of kin favours financial institutions more than the families of the original owners of accounts.

“A bank account shall be classified as dormant if there has been no customer or depositor-initiated transaction in it for a period of one (1) year after the last customer or depositor-initiated transaction. When the account becomes dormant. the bank shall institute controls consistent with its precautionary policies, including surveillance procedures and second level authorisation,” is all CBN says on the matter.

So, when family members are unaware of a savings plan at a financial institution, and the customer dies, it is left to the institution to deal with the assets or monies based on their own internal policy.

In reaction to this, a general partner at Philip, Witte, and Alu Solicitors and Advocates, Philip Nnannah at the inauguration of the House of Representatives Ad-Hoc Committee, in February, to recover Federal Government funds trapped in commercial banks, called on CBN to create a sweeping policy that will compel financial institutions in the country to reach out to next of kins of dormant accounts, especially the ones with funds.

Generally, the question as to who to inherit one’s wealth after demise is determined by law, that is, customary law, Islamic law or English Law or the Administration of Estates Law (or equivalent legislation). And, the law to be applicable in distributing the estate of the deceased shall be determined by the incidence of marriage of the deceased. It follows therefore that where a deceased contracted marriage under the Marriage Act, customary law is excluded, and succession to his wealth will be effected in accordance with either the English law or the Administration of Estates Law (or equivalent legislation), depending on the jurisdiction.

Nigerian lawyer, O. G Chukkol, said a next-of-kin can inherit assets only if he is named in a Will as a beneficiary or by his status he is entitled by law to inherit but not actually because he is named as the next-of-kin of the deceased in a bank or place of work.He went further to state that under the Nigerian law of intestate succession, one cannot choose his heir under the pretext of next-of-kin; the law imposes heirs on him.

Chukkol said, “Are you among those that think by giving a name to financial institutions (bank for example) as next-of-kin you have chosen that person to automatically inherit your wealth in the event of your demise? In other words, do you think by merely picking someone as your next-of-kin you have made that person a beneficiary to your wealth or entitlement(s) in the event of your death?

“Under the Nigerian law of intestate succession, one cannot choose his heir under the pretext of next-of-kin; the law imposes heirs on him. For example, it is the surviving spouse and children of an intestate who married under the Act that are his heirs. The intestate cannot, therefore, by naming only one of them or any of his other blood relatives his next-of-kin, scheme them out of inheritance as the act of naming his next-of-kin does not amount to testamentary disposition.

“There is nothing special about next-of-kin as far as succession is concerned. Next-of-kin is merely the first contact point if anything happens to you. He is someone empowered to make decisions for you in times of emergency or where you are not readily available or unable to make the decisions yourself.

“He is someone empowered to provide necessary information about you where needed such as confirming your identity. He is also someone positioned to make medical decisions such as providing consent for a medical procedure. At best, what a next-of-kin can do after the demise of the deceased is perhaps to ensure that necessary steps are taken towards obtaining a letter of administration from the probate. The typical Nigerian’s conception of the term, “next-of-kin” is therefore erroneous,” he said.

So, with the CBN shelling decisions to companies, it falls on the fintech company to make sure the next of kin receive their inheritance if a customer dies. But many fintech companies haven’t created infrastructure in place that enables this.

Fintech companies are mostly quiet on transfer of assets to next of kin

In a recent survey by Technext of a handful of major fintech players, cutting across savings, investment, cryptocurrency and NFTs, only one company, CowryWise said that it will reach out to the next of kin if an account becomes dormant after a year.

CowryWise defines dormant as “if an account with funds isn’t accessed after a year and/or there’re no inflow or outflow transactions within a full year.”

It said that it will then “reach out to the customer first and only reach the NOK if we do not get a response from our customer.”

On its website, PiggyVest, says that it will reach out to the next of kin after “a long period of time.” But, a chat with a customer relations representative revealed a different internal policy.

“In the case of death, your next of kin can reach out to us. Ideally, they should be aware that you own an account with us and that they are your next of kin,” PiggyVest said on the matter.

When asked about the information on their website that says it will reach out “after a long period of time,” the representative pushed back insisting that “we advise they (next of kin) be aware to enable them have access.”

While PiggyBank, CashBox, CowryWise, and some other fintech companies that were part of the Technext survey have a space for customers to fill in their next of kin details, many cryptocurrency platforms do not have provisions for same.

“Our product team is working on a feature that allows you add a next of kin and we will keep all our users updated once this is available on our platforms,” BuyCoins, a crypto exchange platform that has been in existence since 2017 said.

The million-dollar question

What happens to their coins when customers die without a next of kin or a will?

“The coins remain in the account. In the event that there is any claim on the basis of someone’s death, we evaluate claims and make any necessary decisions,” BuyCoins said.

It added that it is now “working on a feature which allows you provide the details of your next-of-kin and allows us contact them if you have coins but have not used your account in a specific period of time.”

But, Joy Ajike who heads communication at CashBox insists that customers should inform their next of kins of all their savings and investments, especially when they don’t have a will, arguing that the customer base the financial sector has to deal with is enormous, making it difficult to reach out to customers with dormant accounts, or their next of kin.

Many of these fintech companies are in the early stage and don’t have that capacity.

“That is one issue that the financial sector has not really been able to overcome…There is no way the bank will know…With the amount of customer base the financial sector has, I don’t think it is something that you can always be tracking…We can’t exactly start calling each customer and harassing them ‘why are you not saving anymore,'” she told Technext.

Young Nigerians are not keeping their next of kins in the loop

Why are young Nigerians not informing their next of kin of all their savings and investments? For many, just like their parents, it didn’t occur to them that they now have investments and should tell their next of kin about it.

Until you brought it up, I had never even given it a thought at all

Laolu Olagunju, UI/UX engineer

“Nobody was aware. I just did it out of my brain,” Idris, a graphic designer based in Lagos said.

“Young people do not want to show their other sources of income, especially if the next of kin is a parent or older siblings.” Amarachi, who works at a tech company in Lagos said.

The same scepticism that inhibited middle-aged and older Nigerians from disclosing their savings and investments to their next of kin, even as tech offers young Nigerian access to early-stage investments options, is gradually creeping in.

With CBN unwilling to compel financial institutions to be attentive to the next of kin problem, the path to securing their investments is going to be a long one. Except, of course, they tell them (the next of kin), themselves.