Financial inclusion is a crucial goal for many of Africa’s developing countries. In Nigeria, only 67.5 million of the 105.5 million adults have a bank account for financial transactions. This means that 64% of the adults in the country are banked while the remaining 36% are unbanked.

Mobile money operators or Mobile Network Operators (MNO), as the Central Bank of Nigeria (CBN), refers to them are therefore crucial agents in ensuring that more people can perform financial services where the banks are not available.

Mobile money is a service that stores money in a secure electronic account that is linked to a mobile phone number. The service allows people to store, send, and receive money using their mobile phones. With this money, they can buy items offline or online, pay bills, school fees, and top up mobile airtime as well as also withdraw cash from authorised agents.

The major distinction between mobile money services and other forms of banking is that a bank account is not necessary. The only requirement is a basic mobile phone and telephone connection.

Because of the mobile phone number requirement, telecommunication operators have been part of the leading operators in the MoMo space in Africa. In Nigeria, these telco operators include MTN Mobile Money and Airtel Money.

Also Read: Former Safeboda boss, Babajide Duroshola joins M-KOPA as Country Manager to lead Nigerian expansion

However, the telcos’ roles in this space are being redefined by the CBN. In a document, the apex bank released a set of regulations that will guide all activities of mobile money operators in Nigeria.

The framework for mobile money operators

The document reads in part, “The CBN recognizes the importance of Mobile Network Operators (MNOs) in the operations of mobile money services and appreciates the criticality of the infrastructure they provide. However, the telco-led model (where the lead initiator is an MNO), shall not be operational in Nigeria.”

The regulation divides mobile money into two categories which are the Bank-led model and the Non-Bank led model. With the first model, a bank or a consortium of banks can provide mobile money services while the second model provides for non-bank organizations like Paga to render those services.

Whatever the model, the MNOs have to obtain a license from the CBN as well as unique shortcodes and meet Know-Your-Customer requirements in their customer registration processes.

Also Read: VC startup, GetEquity closes $100k pre-seed round to launch its startup funding platform

Based on the new regulations, the operators can create and manage wallets as well as issue e-money. They can also recruit and manage agents and engage in other activities that the CBN permits.

The regulations also state that they can not grant loans, advances and guarantees; accept foreign currency deposits or deal in the foreign exchange market. However, they can carry out payments and remittance services through channels within the country and sell foreign currencies from inbound cross-border remittances to authorized forex dealers.

The growth of mobile money use in Africa has been huge and has spurred regulators into action. Beyond providing a framework for the operators, however, it also brings new limitations to their operations in Nigeria. Here are the major ones.

Protecting Nigerian Banks from MNO’s

Airtime cannot be converted into cash as well by operators in Nigeria. In other countries where MTN Mobile Money operates, users are allowed to convert their airtime into cash. However, allowing telcos to do that will mean that subscribers can recharge airtime and simply spend it as money without paying bank fees.

For instance, MTN’s large customer base of almost 60 million people in Nigeria will give it an advantage that banks do not have because subscribers will be able to transact using airtime and skip bank charges.

In 2020, Businessdaily reports that telcos with mobile money operations made huge gains because of transactions carried out on their network. Nigeria recorded $428 billion worth of e-transactions in 2020, 42% higher than in 2019 while MoMo transactions in Ghana outweighed cheque transactions by $40 billion in Q1 2021, according to a report by Ghanaian ICT industrialist, Eric Osiakwan.

The transactions facilitated in Kenya by M-Pesa rose by 32.9% year-on-year to $82 billion in 2020 and the volume of transactions grew by 14.9%, to 5.12 billion transactions. Orange’s MoMo service also saw an 18.9% increase in active users to a total of 19.6M customers by the end of June 2020.

These trends in Africa show a rising adoption of mobile money and agency banking services because of the convenience they offer. For traditional banks, these numbers are also a cause for worry and may be part of why the CBN has restricted aspects of banking services from being offered by MoMo operators in Nigeria.

New limitations to banking the unbanked

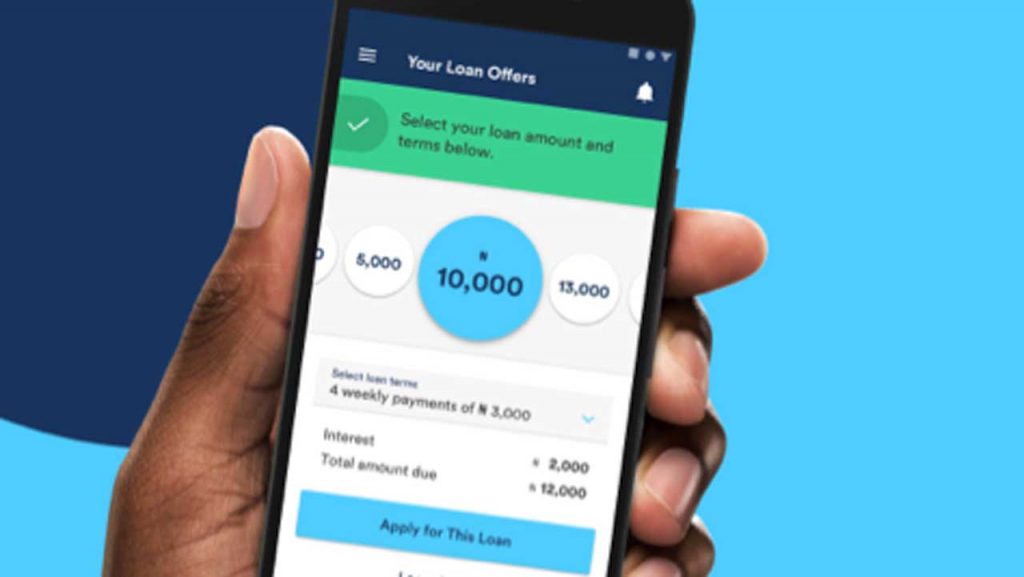

Banking services that people without a bank account do not have access to includes access to credit. As people continue to use mobile money services, they are building a financial record that can be used to determine their creditworthiness and in turn be used to determine whether they are eligible for certain loans or not.

However, this is no longer a possibility because MNOs are not allowed to give loans or guarantee one, meaning that the financial record that each user builds is not useful for lending purposes.

In other countries, like Ghana, MTN MoMo and other MNOs can offer mobile money loans to customers based on their financial worthiness. Users can also request quick loans with or without owning a bank account as long as they have the MoMo pin. This is one of the reasons for the huge growth recorded in the space in Ghana. However, Nigeria does not seem to be towing this part, following the statement by the regulators that the telco-led model will not be operational here.

Possible loss of revenue for mobile money operators

The framework also restricts MoMo operators to their basic functionality which is to provide an alternative way for people to access financial services without a bank account. The restrictions on foreign currency trade mean that operators like Paga will not be able to facilitate outbound remittances of foreign currency for customers. This cuts off any revenue that could be generated from that portion of the business.

While fintechs like Carbon, Paylater, Kiakia and Aella Credit can provide loans to users, mobile money operators like Paga, MTN MoMo, Airtel Money and Firstbank’s Firstmonie will not be able to venture into that space. As earlier mentioned, MTN MoMo provides loans to users in Ghana and generates revenue from that.

The regulations in place over here, however, have nipped that idea and ensures that in that area, MNOs will not be able to compete with banks. As the mobile money space continue to grow, the regulations by the CBN will make sure that the focus is on the basics of financial inclusion and nothing that will bring them into direct competition with the traditional banking sector.